How One Nonprofit Mapped Every Zip Code in America and Discovered That Credit Scores Predict Life Expectancy, Crime Rates, and Homeownership—and Why It Matters for Policy, Practice, and American Renewal

Part I: A Map of Inequality—Drawn from Home

When I drive through the Crenshaw District today—the neighborhood where Operation HOPE was born thirty-four years ago in the aftermath of the 1992 Los Angeles uprisings—I know something now that I didn’t know when we started this work. I can tell you, with precision, what the average credit score is in the 90043 zip code. I can tell you it’s 664. And I can tell you what that number means: it’s a signal. Not a judgment. A signal.

That signal has a language. And Operation HOPE, Inc., working in partnership with Experian, spent years learning to read it.

The Crenshaw district—my birthplace, the place where we founded this organization—is where I first understood that America’s problems are, fundamentally, economic problems. And that our inability to measure the granularity of that economic reality has been part of the reason we’ve failed to solve it. How do you fix what you don’t measure? How do you build a moral economy when you’re flying blind?

In October 2022, Operation HOPE launched the HOPE Community Credit Score Index. For the first time in American history, we had a tool that could map, zip code by zip code, the financial wellness of every neighborhood across the United States. Not a theory. Not a projection. Actual data. The kind of data that tells you the truth about who gets access to capital, who builds wealth, and who gets left behind.

I revealed it first on CNBC’s Squawk Box. And the data didn’t lie. Neither should I.

Part II: The Methodology—What We Measure and Why It Matters

The Index: A Snapshot of Community Financial Health

The HOPE Community Credit Score Index works by doing something that, while simple in concept, had never been done systematically before in America: it overlays resident credit score data—aggregated by zip code—with other critical data on education, homeownership, income, life expectancy, and crime.

The result is a corner-by-corner, block-by-block snapshot of a community’s financial health.

Experian provides the credit data. The Index methodology is built on the principle that credit scores are not merely financial metrics—they are correlates with social, health, and economic outcomes. When you understand that credit is access, and access is power, you begin to understand why a community’s average credit score matters as much as any other health indicator we track.

The variables measured in the Index include:

Credit Score Density — The average credit score within a given zip code; measured on the standard 300-850 scale.

Educational Attainment — High school graduation rates and post-secondary degree completion rates within the community.

Homeownership Rates — The percentage of residents who own their homes, tracked as a proxy for wealth-building capacity and economic stability.

Median Household Income — A measure of earning power and economic participation.

Life Expectancy — The average number of years residents in a given zip code are expected to live.

Crime Rates — Specifically, violent crime per 1,000 residents, tracked as a social stability and safety indicator.

Why These Variables? Why Now?

For decades, policymakers and researchers have studied poverty, inequality, and economic access in isolation. We’ve had separate conversations about education, health, housing, criminal justice, and financial services. What the HOPE Community Credit Score Index does is integrate these conversations around a single, actionable metric: financial wellness.

Credit score is not a moral judgment. It is a measurement of behavior and circumstance. A credit score tells you whether a person can borrow money, at what rate, and whether a bank will take a financial risk on them. It is the single most important gate to the American free enterprise system: mortgages, business loans, car financing, even job opportunities, hinge on credit access and cost.

When you map credit scores zip code by zip code, you are, in essence, mapping access to the American Dream itself.

Part III: The Findings—What the Data Reveals

The HOPE Community Credit Score Index has produced findings so stark, so clear, that they are almost impossible to dispute. And yet, for some reason, we continue to act surprised by them.

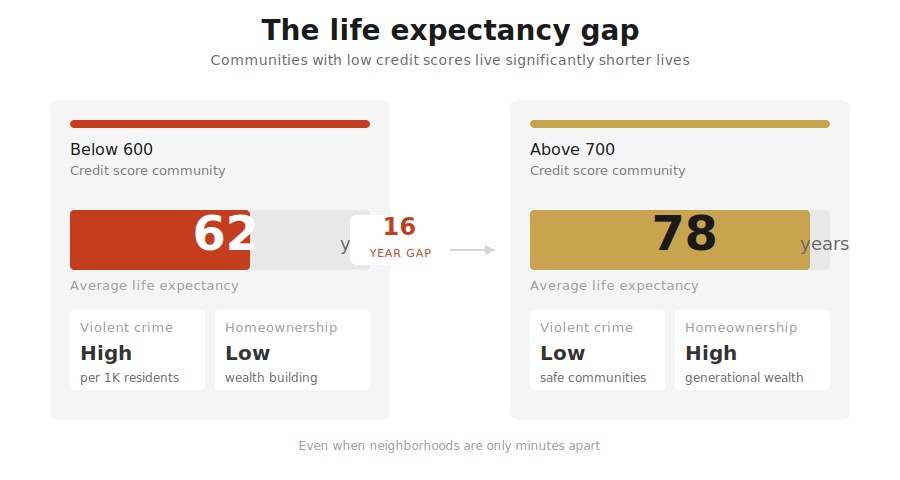

Finding #1: A 15-20 Year Life Expectancy Gap

This is the most visceral finding. Communities with below 600 credit scores tend to have a life expectancy of 15-20 years less than communities with above 700 credit scores—even if these communities are only minutes from each other.

Let me repeat that. Minutes from each other. Same city. Same state. Possibly the same school district, if we’re talking about a sprawling metropolitan area. And yet: a 15-to-20-year difference in how long residents are expected to live.

This is not coincidental. This is not mysterious. This is economic violence, measured in years of life.

When a community has low access to capital, what follows is low access to everything else: healthcare, nutrition, safe housing, stress reduction, preventive care, emergency services that arrive quickly. Chronic stress from financial instability literally shortens your life. This is documented science. This is the somatic cost of exclusion.

The data is not theoretical. Here’s what this gap looks like in a real American city:

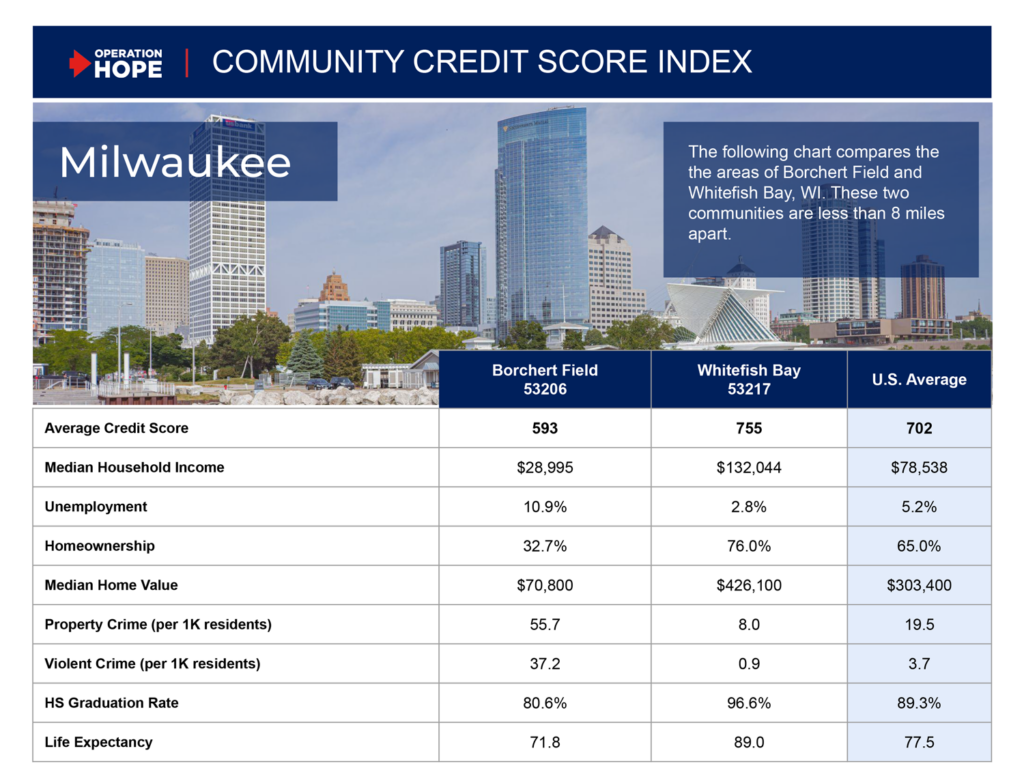

MILWAUKEE, WISCONSIN — BORCHERT FIELD vs. WHITEFISH BAY

These two neighborhoods sit less than 8 miles apart in Milwaukee. They are different worlds.

Borchert Field (zip code 53206) has an average credit score of 593. The median household income is $28,995. Homeownership sits at 32.7%. High school graduation rate: 80.6%. Life expectancy: 71.8 years.

Whitefish Bay (zip code 53217) has an average credit score of 755—a 162-point gap. Median household income: $132,044 (4.6 times higher). Homeownership: 76.0%. High school graduation: 96.6%. Life expectancy: 89.0 years.

The residents of Whitefish Bay can expect to live 17.2 years longer than their counterparts in Borchert Field. Not because of genetics. Not because of personal choices alone. Because of access. Because of capital. Because of a credit score.

Property crime in Borchert Field: 55.7 per 1,000 residents. In Whitefish Bay: 8.0. Violent crime: 37.2 vs. 0.9 per 1,000 residents. The median home value: $70,800 vs. $426,100.

Unemployment in Borchert Field: 10.9%. In Whitefish Bay: 2.8%.

These neighborhoods are not separated by geography or history alone. They are separated by access to capital—and that separation translates into almost every outcome we care about.

The 700 credit score threshold—the target of our HOPE 700-Credit-Score-Communities initiative—is not an arbitrary number. It is the score at which borrowing becomes affordable, reliable, and real. It is the score at which you can participate.

Finding #2: Violent Crime Density Correlates with Low Credit Scores

Communities with below 600 credit scores tend to have very high ‘violent crimes per 1K residents’ ratios.

Again, this is not a moral statement about the people who live in these neighborhoods. This is a statement about desperation, about the absence of economic hope, about what happens when young people see no pathway to wealth-building through legitimate means.

When a young person in a 600-score neighborhood looks around and sees that credit is not available to their parents, that homeownership is out of reach, that starting a business requires capital they don’t have—what else do you expect them to do? You are watching the rational response to systemic exclusion. The crime is not the robbery. The crime is the system that makes robbery the only visible path forward.

Here’s what this looks like in Washington, D.C.:

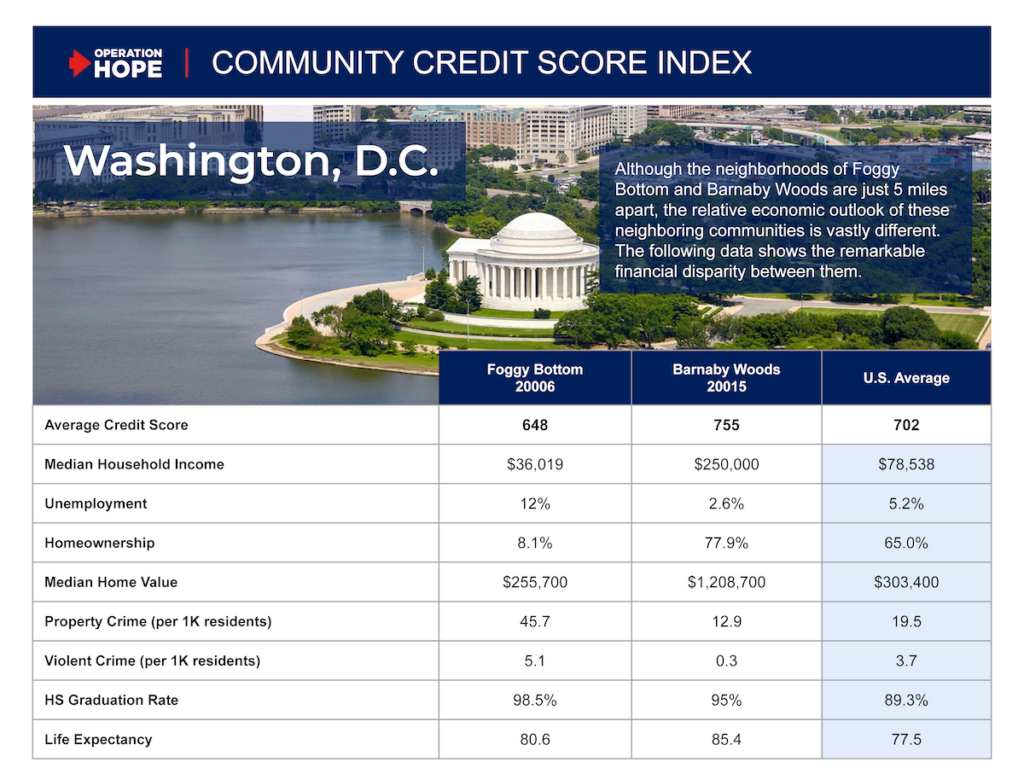

WASHINGTON, D.C. — FOGGY BOTTOM vs. BARNABY WOODS

Although the neighborhoods of Foggy Bottom and Barnaby Woods are just 5 miles apart in Washington, D.C., the relative economic outlook of these neighboring communities is vastly different.

Foggy Bottom (zip code 20006) has an average credit score of 648. Median household income: $36,019. Homeownership: 8.1%. Unemployment: 12%. Life expectancy: 80.6 years.

Barnaby Woods (zip code 20015) has a credit score of 755. Median household income: $250,000 (nearly seven times higher). Homeownership: 77.9%. Unemployment: 2.6%. Life expectancy: 85.4 years.

But the crime statistics tell the starkest story.

Violent crime in Foggy Bottom: 5.1 per 1,000 residents. In Barnaby Woods: 0.3 per 1,000 residents. That’s 17 times higher violent crime in the lower-credit-score neighborhood—5 miles away from one of Washington’s most affluent areas.

Property crime: 45.7 vs. 12.9 per 1,000 residents.

This is what economic exclusion looks like on the ground. Young people in Foggy Bottom are not inherently more prone to crime. They are responding to an environment where legitimate economic pathways have been closed off. They see homeownership at 8% in their neighborhood and 78% across town. They see unemployment at 12% while it’s 2.6% in neighborhoods they can see from their blocks. The rational response to that disparity is desperation.

Finding #3: Homeownership and Educational Attainment Follow the Credit Score Gradient

Communities with below 600 credit scores tend to have low home ownership rates and low rates of high school graduations.

This finding reveals the intergenerational trap. Low credit scores mean no mortgages. No mortgages mean no home equity. No home equity means no down payment for your child’s college, no collateral for a small business loan, no safety net. You are stuck.

Meanwhile, in the high-credit-score neighborhoods—the 750+ zip codes—residents are building wealth through home equity, using that equity to educate their children, using education to increase their earning power, using earnings to improve credit, using credit to build more wealth. This is the compound interest of opportunity.

The inverse—what we see in low-credit-score neighborhoods—is the compound interest of exclusion.

This pattern is visible in every region of America. Look at Fayetteville, North Carolina:

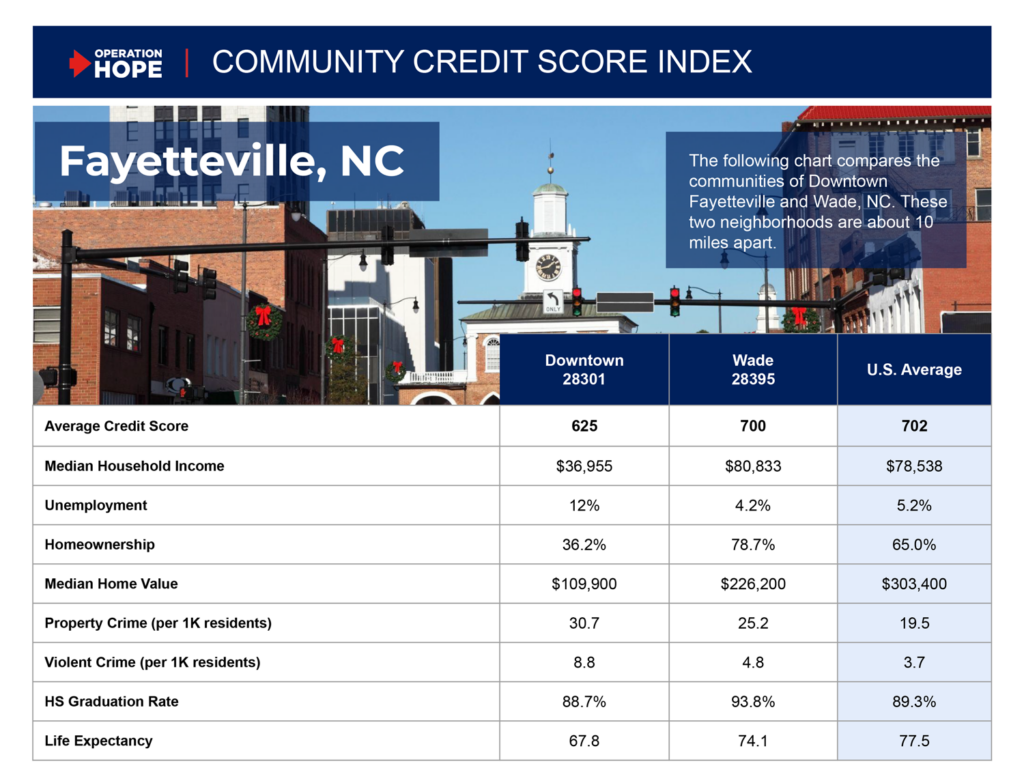

FAYETTEVILLE, NORTH CAROLINA — DOWNTOWN vs. WADE

Downtown Fayetteville (zip code 28301) and Wade (zip code 28395) are about 10 miles apart. They might as well be on different planets.

Downtown Fayetteville: average credit score 625. Median household income: $36,955. Unemployment: 12%. Homeownership rate: 36.2%. High school graduation rate: 88.7%. Median home value: $109,900. Life expectancy: 67.8 years.

Wade: average credit score 700. Median household income: $80,833 (more than double). Unemployment: 4.2%. Homeownership: 78.7%. High school graduation: 93.8%. Median home value: $226,200. Life expectancy: 74.1 years.

The homeownership gap is stark: 36% in Downtown Fayetteville, 79% in Wade. That’s the difference between building generational wealth and staying on the treadmill. A parent in Wade can use their home equity to send their child to college. A parent in Downtown Fayetteville has no such option. Their child will inherit debt, not assets.

And the high school graduation rates: 89% vs. 94%. That 5-percentage-point gap compounds over a generation.

Finding #4: Income Disparities Are Stark and Measurable

While income data alone doesn’t tell the whole story, the Index reveals disparities within the same city that are staggering. These gaps exist not between different regions, but within one city. Often within sight of each other.

In Gallup, New Mexico—about 20 miles separate two different economic universes:

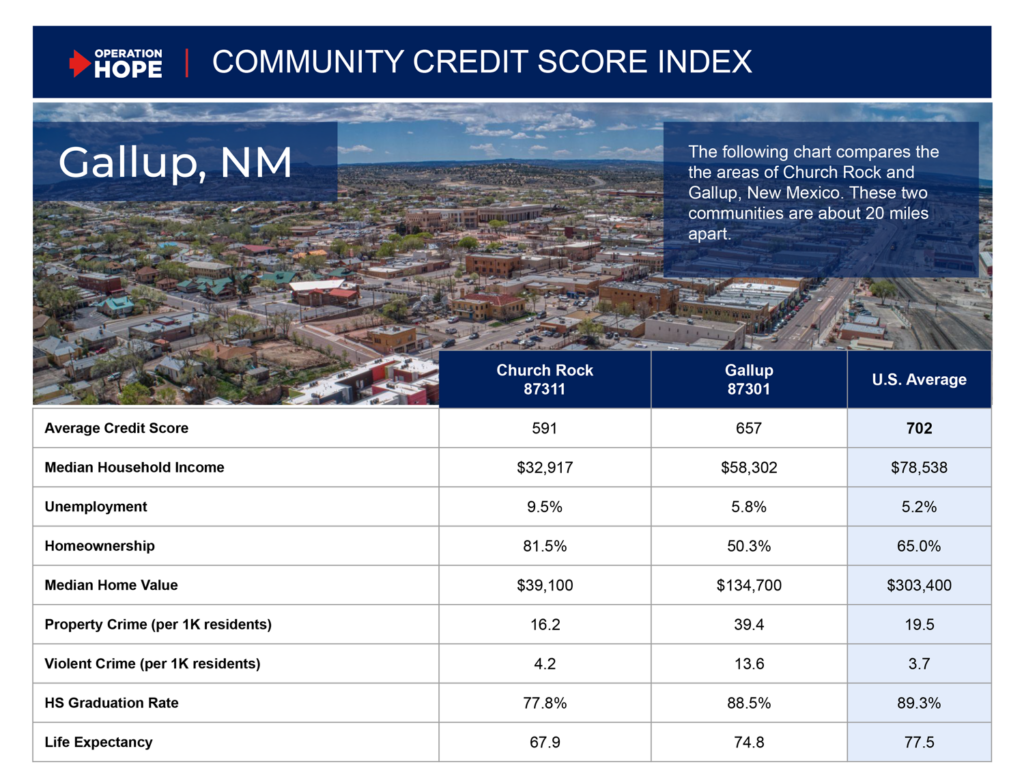

GALLUP, NEW MEXICO — CHURCH ROCK vs. GALLUP

Church Rock (zip code 87311) and Gallup (zip code 87301) are about 20 miles apart in New Mexico.

Church Rock: average credit score 591. Median household income: $32,917. Unemployment: 9.5%. Homeownership: 81.5%. High school graduation: 77.8%. Median home value: $39,100. Life expectancy: 67.9 years.

Gallup: average credit score 657. Median household income: $58,302 (77% higher). Unemployment: 5.8%. Homeownership: 50.3%. High school graduation: 88.5%. Median home value: $134,700. Life expectancy: 74.8 years.

The income story: $32,917 vs. $58,302. In Church Rock, that gap means the difference between having enough to eat and rationing. It means healthcare decisions based on cost, not health. It means your child’s educational trajectory is determined before they’re born.

The credit score gap—66 points—translates directly into access to capital. A person in Church Rock cannot borrow to start a business, cannot get a reasonable mortgage rate, cannot build wealth. A person in Gallup can.

Part IV: The Larger Context—What This Means

What do these findings tell us? They tell us that the HOPE Community Credit Score Index has mapped American inequality with precision. And the precision is damning.

It shows us that:

Zip code predicts credit score. Credit score predicts access to capital. Access to capital predicts income. Income predicts homeownership. Homeownership predicts education. Education predicts life expectancy.

In other words: where you’re born predicts how long you’ll live.

This is not acceptable in a nation that claims to believe in equal opportunity.

Part V: The Work on the Ground—Operation HOPE’s Response

Understanding the problem is only half the battle. The Index was always meant to be a tool for change, not just a document of despair.

Operation HOPE, through its network of 1500+ physical and satellite locations nationwide—co-located in banks, community centers, and nonprofit spaces—has made it our mission to address these disparities corner by corner, zip code by zip code.

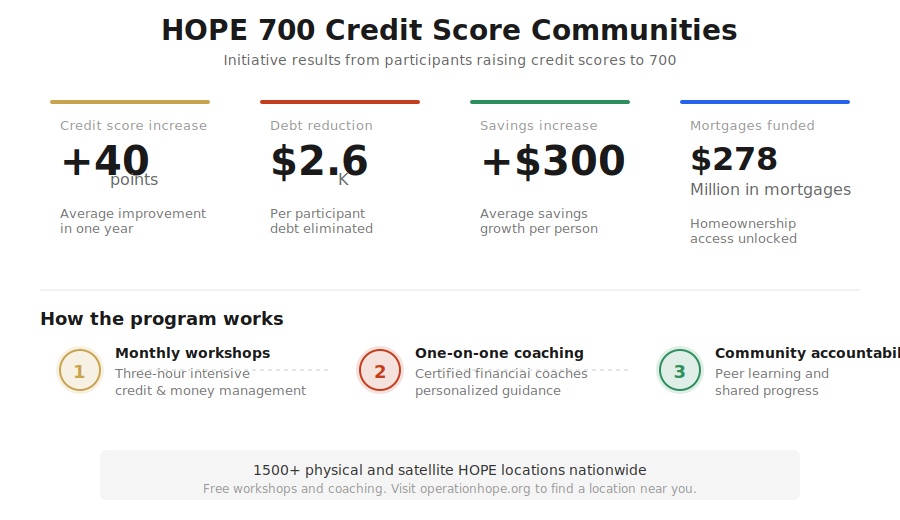

The HOPE 700-Credit-Score-Communities Initiative

The 700-Credit-Score-Communities initiative is our direct response to the Index data. It is built on a simple principle: if we can move people from a credit score of 650 to a credit score of 700, we change their life trajectory. We unlock their access to capital. We give them a seat at the table of American capitalism.

Here’s what the program looks like:

Three-Hour Monthly Workshops — At HOPE Inside locations in neighborhoods with low community credit scores, we hold intensive three-hour workshops on one Saturday morning each month. These are not theoretical exercises. They are practical, hands-on training in credit management, debt reduction, budget-building, and financial strategy. They are free. They are available to everyone.

In the Crenshaw district—where the average credit score in zip code 90043 is 664—these workshops are being led by our financial coaches, reaching residents and small business owners who have been systematically excluded from capital access for generations.

One-on-One Financial Coaching — Workshop participants can schedule private coaching sessions with trained, experienced financial coaches. These are relationship-based interventions. A coach will sit down with you and help you understand your specific financial situation. We don’t shame. We don’t judge. We problem-solve.

HOPE Inside programming includes credit and money management inclusive of various consumer credit counseling certifications such as Consumer Financial Protection Bureau (CFPB) and FDIC, among others. Our coaches are certified. They know the system. And they know how to help people navigate it.

Peer Learning and Accountability — One of the most powerful aspects of this work is what happens when people in the same neighborhood, facing the same barriers, come together and decide to improve their financial health at the same time. It creates accountability. It creates hope. It creates momentum.

The Results: What Improvement Looks Like

The question people always ask: does this work?

Yes. Just last year, Operation HOPE raised participants’ credit scores by an average of 40+ points, moving its clients toward the target of a 700-credit score that transforms individuals’ ability to fully participate in the free enterprise system.

Let me unpack that. A 40-point increase in credit score—that’s the difference between a denial and an approval. That’s the difference between a 7% APR and a 4.5% APR. Over the life of a 30-year mortgage, that’s tens of thousands of dollars. That’s your child’s college fund. That’s your retirement.

Operation HOPE also helped clients reduce debt by an average of $2,600 per client, increase savings by an average of $300 per client in one year, and obtain more than $278 million in funded mortgages.

$278 million in mortgages. That is homeownership. That is wealth-building. That is generational change.

Part VI: Why This Matters—The Intellectual and Moral Case

Financial Literacy Is a Civil Rights Issue

This is where I want to be crystal clear, because this is the throughline of all of Operation HOPE’s work, and it is the core argument of my book Capitalism for All.

Financial literacy is not a nice-to-have. It is not a personal finance tip for people who have disposable income. It is a civil rights issue. It is about access. It is about power. It is about who gets included in the American economy and who gets left out.

When we refuse to teach people—systematically, consistently, as a public good—how to build credit, manage debt, understand mortgages, and access capital, we are making a choice. We are choosing exclusion. And that choice has consequences measured in dollars, in years of life, in crime rates, in generational poverty.

The HOPE Community Credit Score Index proves this. It proves that financial wellness is not disconnected from other forms of wellness. It is foundational. Everything else—health, safety, education, longevity—flows from it.

The “Economic Plumber” Metaphor

I often use the metaphor of a plumber to describe this work. When there’s a leak in a building’s pipes, you don’t call a therapist. You call a plumber. The leak is a systemic problem, not a personal one. It requires a technical solution, not moral exhortation.

America’s financial infrastructure is broken. We have created a system in which entire neighborhoods are locked out of capital. We have allowed zip codes to become destiny. We have tolerated a situation in which your life expectancy is determined by your credit score, which is determined by your zip code, which is often determined by the color of your skin and the economic status of your parents.

This is not a psychological problem. This is a plumbing problem. And it requires a plumber—or in this case, an economic empowerment organization—to fix it.

The HOPE Community Credit Score Index is the diagnostic tool. HOPE Inside locations are where the repair work happens.

Part VII: What the Index Tells Us About Policy

The HOPE Community Credit Score Index has implications far beyond Operation HOPE’s work. It is a tool for policymakers, researchers, academics, and civic leaders.

For Municipal Leaders

If you are a mayor, a city council member, or a municipal planner, the Index tells you where your community is vulnerable. It tells you which zip codes need intervention, which ones are in crisis, and which ones are on an upward trajectory. It provides a metric for success—not just employment, not just crime reduction, but financial wellness.

The Index can inform resource allocation. It can direct investment. It can help you understand whether your economic development policies are actually working.

For Researchers and Academics

The HOPE Community Credit Score Index is an open invitation for rigorous study. We’ve provided the data. We’ve shown the correlations. Now we want researchers to dig deeper. Why does credit score correlate with life expectancy? What are the causal mechanisms? Can targeted credit-building interventions reduce crime? Do they improve health outcomes?

These are not rhetorical questions. They are empirical ones. And they deserve serious research.

For Corporate and Institutional Partners

For financial institutions, employers, and large corporations, the Index is a wake-up call. If you are serious about inclusive capitalism, if you are serious about narrowing economic gaps, you cannot afford to ignore the zip codes where the average credit score is below 600. That is where your talent is. That is where your customers are. That is where your market growth is. And right now, you are not reaching them.

Banks can partner with Operation HOPE, as U.S. Bank and others have done, to co-locate HOPE Inside locations and provide free financial coaching. Employers can offer financial wellness programs to their workforce. Corporations can invest in credit-building initiatives in their communities of operation.

The economics are clear: a person with a 700 credit score is a better customer, a more stable employee, and a more engaged community member.

For Policymakers at the Federal Level

Finally, to members of Congress, to the Administration, to the Federal Reserve: the HOPE Community Credit Score Index is evidence. It is proof that economic inclusion is not just a moral good—it is a measurable, empirical outcome that affects every other metric we care about: health, crime, education, social mobility.

The Index argues for the following policies:

- Universal Financial Literacy Education — From high school onward, every young American should receive rigorous, hands-on financial literacy education. This should include credit, debt, budgeting, investing, and entrepreneurship. It should be mandatory, just like math and English.

- Community-Based Financial Coaching Infrastructure — We need a nationwide network of financial coaching centers, similar to our HOPE Inside locations, accessible to every community. These should be funded publicly, like libraries or public schools, because financial wellness is a public good.

- Community Reinvestment Accountability — Banks must be held accountable for serving low-credit-score communities. The Community Reinvestment Act exists for a reason. It should be strengthened, not weakened.

- Equitable Lending Standards — Predatory lending disproportionately targets low-credit-score neighborhoods. We need regulatory oversight to ensure that credit is available at fair rates to people trying to build their scores, not locked behind payday loans and title loans.

Part VIII: The Larger Vision—Capitalism for All

This work—the Index, the 700-Credit-Score-Communities initiative, the HOPE Inside locations—is not separate from the larger work of inclusive capitalism that I write about in Capitalism for All: Inclusive Economics and the Future-Proofing of America.

The argument is simple: America’s future depends on our willingness to include everyone in the economy. Not out of charity. Out of self-interest. Out of math.

When you lock a zip code out of capital, you lose the entrepreneurship that would have emerged there. You lose the innovation. You lose the consumption. You lose the tax revenue. You lose the stability. You don’t gain anything. You just make society smaller and more brittle.

The HOPE Community Credit Score Index proves this. It shows you, in data, what happens when you exclude people from capitalism: they die earlier, they commit more crimes, they own fewer homes, they educate their children less. Not because they are different. But because they are excluded.

The opposite should also be true: include people, give them access, provide them with the tools and knowledge to build credit and wealth, and you get life expectancy increases, crime reductions, homeownership, education, stability, and growth.

That is capitalism for all. That is what we are building.

Part IX: The Work Continues

We have 1500+ physical and satellite locations today across the nation. We are in conversations with federal agencies, major corporations, universities, and municipalities about continued expansion and deepening of our impact.

But I will be honest: we can expand a thousand times over and still not reach everyone who needs this work. The scale of the problem—zip codes across America locked out of capital—is enormous. The solution requires not just Operation HOPE, but a nationwide commitment to financial inclusion.

I invite researchers, academics, policymakers, business leaders, and citizens to use the HOPE Community Credit Score Index. Study it. Question it. Improve it. Most importantly, use it to build the case for change in your community.

The data is clear. The need is urgent. The solution is within reach.

What we lack is not information. We lack will.

Appendix: How to Access the HOPE Community Credit Score Index

The HOPE Community Credit Score Index is publicly available. You can look up your zip code, your neighborhood, your community and see the data for yourself. See how your community’s credit score compares to neighborhoods nearby. See what the correlations tell you about life expectancy, crime, homeownership, and education.

This is data for everyone. Researchers, policymakers, academics, journalists, citizens. Use it. Learn from it. Act on it.

Visit: operationhope.org for access to the HOPE Community Credit Score Index and to find a HOPE location near you.

About the Author

John Hope Bryant is Founder, Chairman, and CEO of Operation HOPE, Inc., the nation’s largest nonprofit dedicated to financial empowerment for underserved communities, and author of Capitalism for All: Inclusive Economics and the Future-Proofing of America. He is a longtime advocate for financial literacy as a civil rights issue and inclusive capitalism as the pathway to American renewal.

All: Inclusive Economics and the Future-Proofing of America — Available now at all major booksellers.

John Hope Bryant — founder of Bryant Group Ventures, Operation HOPE, Inc, publisher of the Bryant Journal and author of his 7th book Capitalism for All: Inclusive Economics and the Future Proofing of America, now a bestseller. Bryant was recently named a member of the Forbes 250.